Inference for Generalized Multivariate Analysis of Variance (GMANOVA) models, under Multivariate Skew t distribution for skewed and heavy-tailed data

Conference

64th ISI World Statistics Congress - Ottawa, Canada

Format: CPS Poster

Session: CPS Posters-03

Monday 17 July 4 p.m. - 5:20 p.m. (Canada/Eastern)

Abstract

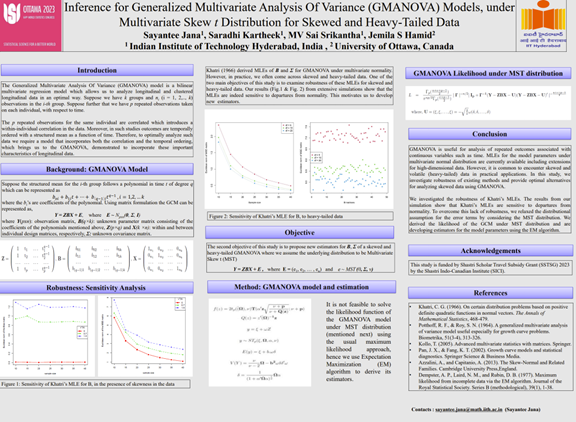

The most extensively used statistical model in practice, both in research and in practice, is the linear model, due to its simplicity and interpretability. Linear models are preferred, even when approximate, for both univariate and multivariate data, especially since, multivariate skewed models come with their own added complexity. Hence, researchers would not prefer to deliberately add extra layers of complexity by considering non-linear models. Generalized Multivariate Analysis of Variance (GMANOVA) models, is one such linear model useful for the analysis of longitudinal data, which is repeated measurements of a continuous variable, from several individuals across any ordered variable such as time, temperature, pressure etc. It consists of a bilinear structure which allows for comparison across between groups, while maintaining the temporal structure of the data, unlike the Multivariate Analysis of Variance (MANOVA) which does not allow for any temporal ordering or temporal correlation in the model. GMANOVA models are widely used in economics, social and physical sciences, medical research and pharmaceutical studies. However, despite financial data being time-varying, the traditional GMANOVA model has limited to no applications in finance, due to the skewed and volatile nature of such data. This in turn makes financial data the right candidate for Multivariate Skew t (MST) distribution, as it allows for outliers in the data to be modelled, due to its heavy tails. In fact, portfolio analysis including mutual funds, capital asset pricing are all modelled using elliptical distributions, especially multivariate t distribution. The classical GMANOVA model assumes multivariate normality, and hence inferential tools developed for the classical GMANOVA model, may not be appropriate for skewed and heavy-tailed data. In our study, we develop inferential tools for the GMANOVA model under the MST distribution, so that they can be applied to skewed and volatile data.